ARR Is Broken.

How creative ARR is damaging for both founders and investors and what we look for instead.

ARR used to be a reliable metric for performance and future outlook. With climbing valuations and creative math, it has become a confused signal.

Over the last 18 months, the industry has seen staggering numbers emerge. But as the numbers grow, the business underneath gets harder to read.

Tom Blomfield put the scale of the shift into perspective:

The bar moved dramatically upward at the exact moment the metric used to measure it became more elastic. Taking ARR at face value is no longer a reliable signal for evaluating early-stage startups. In the current market, ARR should be treated as a starting point for questions, not an answer.

The Growth That’s Real

Some of this growth is genuine, and it’s unlike anything we’ve seen before. Stripe’s 2025 annual report found that double the number of new startups hit $10M ARR within three months in 2025 compared to 2024. a16z data shows that the median enterprise AI company now reaches $2M ARR in its first year, raising a Series A just nine months post-monetization. Before AI, $1M ARR in year one was considered best-in-class.

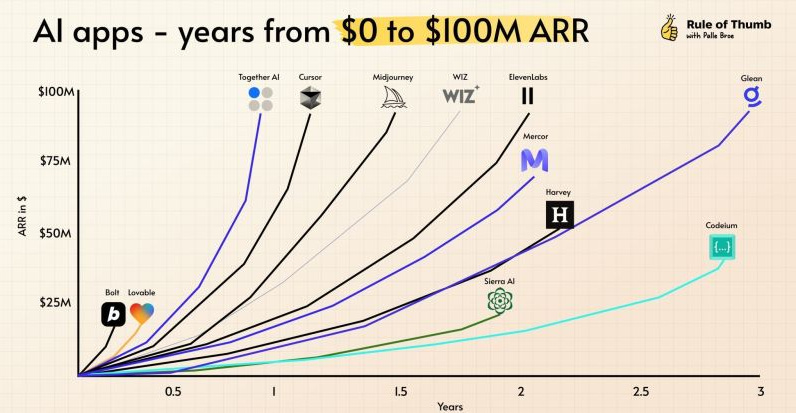

AI is compressing startup lifecycles at a staggering pace with faster development, deployment, and scaling. Cursor went from zero to $100M ARR in a year. Lovable hit the same milestone within months of launch. Wiz sold for $32B. Anthropic, founded in 2022, recently hit a $30B revenue run rate. Harvey and Legora, in the same legal AI sector, show similarly explosive trajectories.

The impressive growth of these companies deserves acknowledgment. But alongside the real growth, founders are getting increasingly creative with how they portray it, and the speed of genuine growth makes inflated growth much harder to detect. When real $100M ARR years are happening, a fabricated $10M ARR claim looks almost conservative by comparison.

The signal has become both faster and noisier, simultaneously.

The problem isn’t that growth has accelerated. Rather, it’s how genuine acceleration has made it easier for the companies performing the acceleration on paper, rather than living it in reality, to go undetected. That’s not only dangerous for investors seeking reliable signals, but also damaging for the founders doing it.

The flexible “ARR”

ARR used to mean something precise. In the SaaS era, there were agreed conventions: annual per-seat pricing, clear separation between signed contract value and recognized revenue, and a predictable 80-90% conversion from contract to actual booked revenue. The metric wasn’t perfect, but it was at least honest.

AI broke the convention, and now there’s a new playbook for bending it:

Annualizing a single good month

Take your best week, extrapolate to a month, and multiply by twelve. One customer goes viral, one enterprise runs a trial, one usage spike hits, and suddenly you have “ARR.” A founder could claim $325K in ARR based on a single two-week pilot, citing “good authority” that the customer will keep paying. An impressive number, but a significant extrapolation.

Counting pilots as recurring

Trials, proof-of-concept, and Letters of Intent (LOI) are being recorded as “booked ARR” based on what customers might pay, even when contracts allow cancellation at any time. An LOI is an expression of interest, not a contract, and there is no billing attached or renewal obligations.

There is preliminary or possible revenue, but no guarantee of recurrence.

AI inference spikes as revenue:

Many companies, particularly in AI, see enormous usage spikes when a customer experiments with a new tool. Companies are trying products, not committing to them. When the experiment ends, the revenue ends with it. Altimeter investor Jamin Ball has called this “experimental recurring revenue”, and many AI companies, seeing monthly churn rates of 10–15% rather than the traditional 5–7%, are running hard just to replace what they’re losing.

Which brings us to the real driver behind all of this.

AI created a handful of genuinely extraordinary growth stories, and those stories set a new benchmark that the entire market started chasing. Investors began demanding revenue signals at increasingly earlier stages, and founders heard an underlying message: “if you’re not growing like Anthropic/Cursor/Lovable what are you doing?”

Founders responded by finding ways to tell that story with the numbers they had, seeking to stay relevant in a market that had decided extraordinary was the new baseline. The uncomfortable question that follows is whether investors, having created that pressure, are now asking rigorous enough questions on the other side of the table. Most are not.

Why This Hurts Founders Most

This isn’t only an investor problem. It is actively damaging the founders doing it, and the industry is largely overlooking that.

Here’s an increasingly common scenario:

A founder raises on the back of an extrapolated ARR number. Twelve months later, the trials have churned, the usage spike didn’t repeat, and they’re sitting on a cap table priced for a company they haven’t yet built. The round that felt like validation becomes a trap, and now they’re struggling to meet the expectations a metric-obsessed market helped them set for themselves.

The a16z principle of “maximize the business, not the metric” is particularly relevant to this scenario, and to the growing trend of inventive ARR.

A reliable ARR is based on a solid business activity - a specific customer behavior or marketing lever that can be pinpointed and maximized to build out a reliable revenue model.

Momentum-based revenue numbers don’t have that gravity, and founders who report it as recurring aren’t just misleading investors; they’re also setting themselves up for failure. A founder who raised $4M at $25M on the back of annualized trial revenue now has 18 months to prove what was implied. If the trials churn, which AI trials frequently do, they face a down-round narrative at the worst moment, revealing just how high the bar was set.

They’re building a false picture of their own company’s health, extending a runway toward a wall that will eventually stop them.

What We Look At Instead

At Demo Day, ARR is now more of a marketing number than a reliable metric. As genuine AI growth stories set extraordinary benchmarks, Demo Day became a competitive performance as much as a business presentation. Founders learned that strong ARR captured investor attention more immediately than their deeper pitch, and the number stopped being primarily a reflection of business reality and started being engineered for the room.

Accelerators refined the pitch. Investors rewarded the signal. The gap between what ARR claimed and what it actually represented has become wider with every batch, and ARR today tells an investor relatively little on its own.

ARR should be the starting point for investors, opening the conversation to dig deeper into the numbers.

Here is what the conversation needs to cover:

Cohort retention

Real proof of demand: how did the customers acquired in month one behave later on? A company with $800K ARR and 95% month-six retention is a fundamentally different investment than one with $1.2M ARR and 40% churn. The first number might be smaller, but the business is better.

CAC payback period

How long does it take to recover the cost of acquiring a customer? The top-quartile benchmark for $1-5M ARR SaaS companies is five months. Above twelve is a warning. Most founders undercount CAC significantly, excluding founder time, customer success costs, and post-sale overhead. The real number is often two to three times what appears in the deck, and the gap tells you something important about how clearly a founder understands their own unit economics.

Cash collected vs. ARR claimed

The simplest stress test. What actually landed in the bank? The gap between claimed ARR and actual cash collected is precisely where the creative accounting lives.

Digging deeper beneath the surface-level ARR exposes the foundations of the business, and this is where the true signal lies. A founder who can tell us exactly which action grew ARR last month, and explain why that action will work again next month, is building something durable. A founder who can only give us the number is optimizing the metric, not the business.

Skepticism vs. Diligence

The bar moved from $150K to $800K–$2M at Demo Day, powered by technology and compressed lifecycles. Some of those numbers are extraordinary and real. Some are the same business, described more creatively.

Creative ARR is making an already noisy signal noisier. Identifying the real from the exaggerated is exactly what we spend our time doing, because at the prices being paid today, investors cannot afford to get that wrong.

In this market, investors have to ask how the numbers were calculated, what churned, where the growth indicator is, and how that shapes future forecasts. Those aren’t skeptics’ questions. They’re the only questions that reliably separate the companies building something durable from the ones running out of time to find it. They are the questions necessary to separate the companies building something durable from the ones running out of time to find it.

ARR tells you what a founder wants you to believe. Unit economics tell you what’s actually true.

We read both, but only trust one.

Visit lobstercap.com for more.

This. We‘ve stopped taking calls from some VCs because of this.

Exactly!